Cross-Border Payments: How They Work, Types & What Indian Businesses Need to Know

If your business buys from overseas suppliers, sells to international customers, or pays remote freelancers abroad, you’re already dealing with cross-border payments. Understanding how these payments work can help reduce costs, improve settlement times, and ensure regulatory compliance.

What Are Cross-Border Payments?

Cross-border payments are financial transactions where money is transferred between individuals, businesses, or institutions located in different countries. These payments can involve currency conversion, international banking networks, compliance checks, and regulatory requirements before funds reach the recipient.

The global cross-border payments market is projected to grow from $193.5 billion in 2026 to $312.1 billion by 2033, reflecting the increasing demand for international trade, eCommerce, and digital payment solutions.

How Do Cross-Border Payments Work?

A cross-border payment typically follows these steps:

1. The sender initiates the payment through a bank, payment gateway, payment processor, or digital payment platform.

2. Currency conversion occurs if the sender and recipient use different currencies.

3. Compliance and fraud screening checks are performed.

4. The transaction moves through international payment networks.

5. The recipient receives the funds in their local currency or designated account.

Types of Cross-Border Payments

🔹B2B Payments: Businesses paying international suppliers, vendors, or service providers.

🔹B2C Payments: Businesses sending refunds, incentives, or payouts to customers abroad.

🔹C2B Payments: Customers purchasing products, subscriptions, or services from foreign businesses.

🔹P2P Payments: Individuals sending money internationally for remittances, family support, or personal transfers.

🔹Marketplace & Freelancer Payments: Platforms and businesses paying freelancers, contractors, creators, and sellers in different countries.

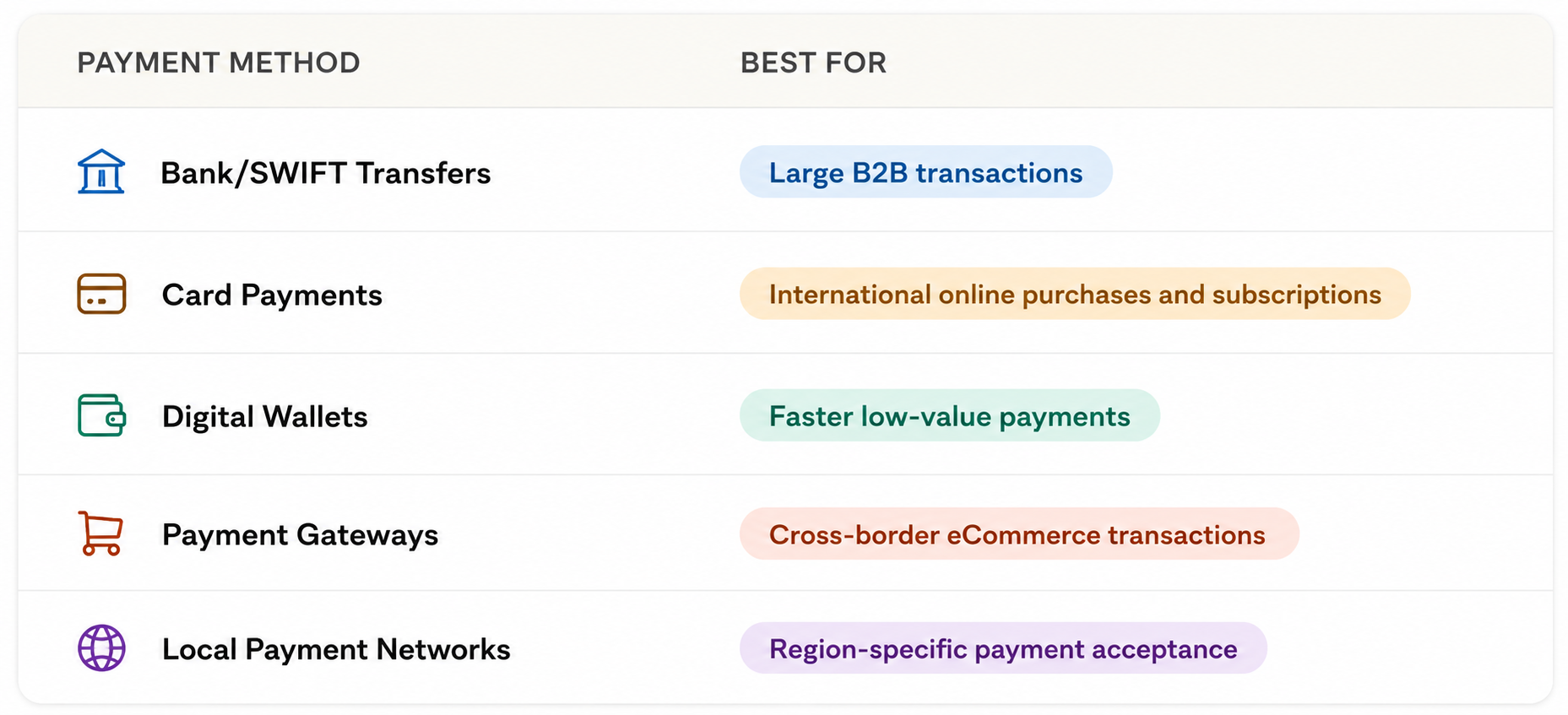

Common Cross-Border Payment Methods

From SWIFT transfers to digital wallets, different cross-border payment methods serve different business and customer needs.

Benefits of Cross-Border Payments

✅ Enable global business expansion

✅ Support international supplier and customer payments

✅ Improve access to global markets

✅ Facilitate freelancer and contractor payouts

✅ Diversify revenue streams internationally

Challenges of Cross-Border Payments

⚠️ Higher transaction fees

⚠️ Currency exchange risks

⚠️ Longer settlement times

⚠️ Complex regulatory compliance

⚠️ Increased fraud and security risks

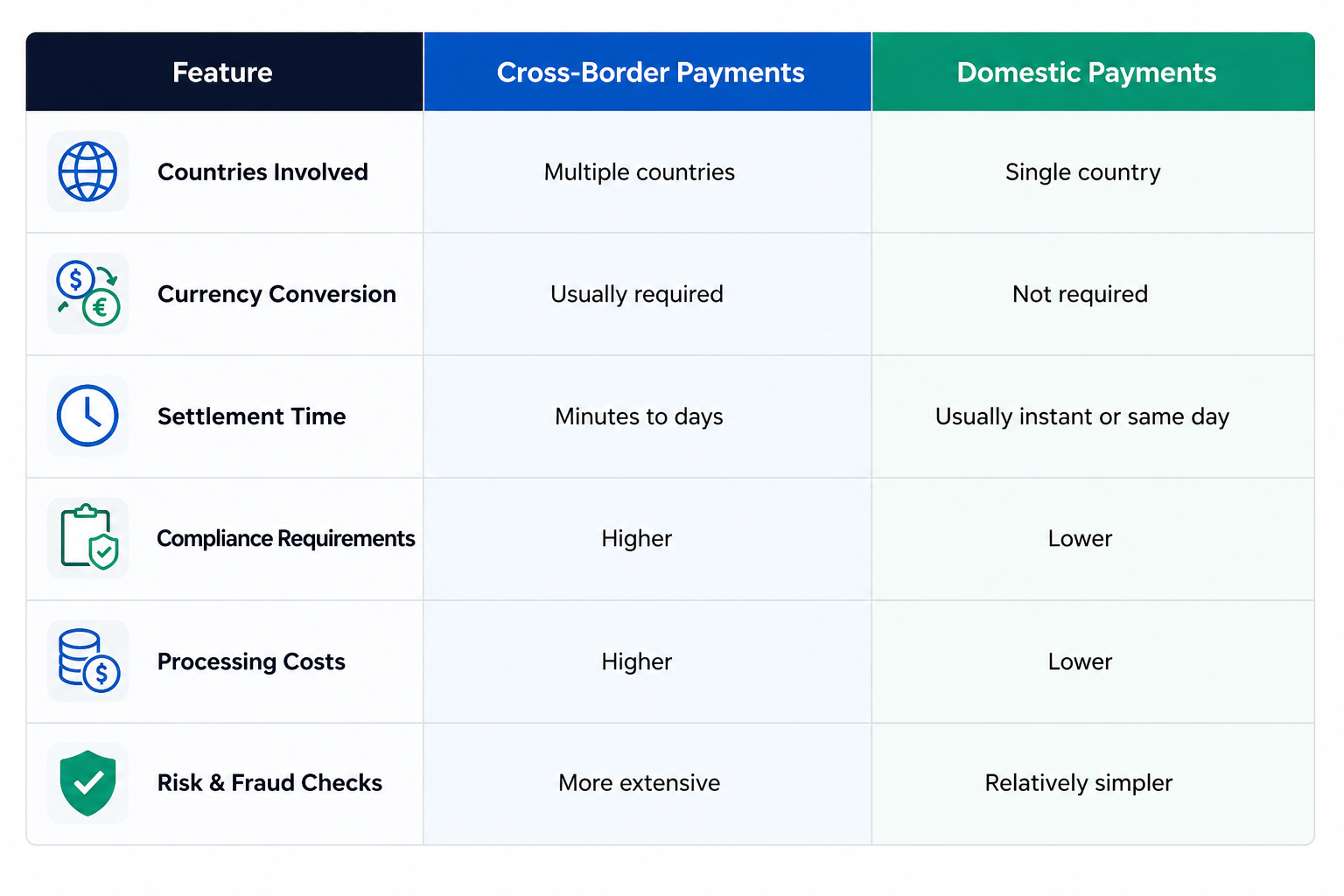

Cross-Border Payments vs Domestic Payments

Understanding the key differences between cross-border and domestic payments is essential for businesses managing both local and international transactions.

RBI & FEMA Regulations for Indian Businesses

Indian businesses handling international payments must comply with:

RBI Guidelines

The Reserve Bank of India regulates international payment activities and foreign exchange transactions.

FEMA Regulations

The Foreign Exchange Management Act governs how money enters and leaves India.

Liberalised Remittance Scheme (LRS)

Allows eligible resident individuals to remit funds abroad within prescribed limits and approved purposes.

Documentation Requirements

Maintain invoices, contracts, tax records, and transaction documents to avoid payment delays and compliance issues.

The Future of Cross-Border Payments

According to industry forecasts, the cross-border payments market is expected to grow at a 7.1% CAGR between 2026 and 2033, driven by real-time payment infrastructure, digital wallets, and increasing global commerce.

The industry is moving toward:

* Real-time international payments

* AI-powered fraud detection

* Faster settlement infrastructure

* Improved payment transparency

* Digital-first payment platforms

* Lower transaction costs

As global commerce grows, businesses increasingly need secure, scalable, and compliant cross-border payment solutions.

Conclusion

Cross-border payments are essential for businesses operating in a global economy. Whether you’re paying overseas suppliers, accepting international customer payments, or managing freelancer payouts, understanding payment methods, compliance requirements, costs, and risks can help you optimize international transactions and support business growth.

Looking to simplify global payments? Explore how a modern cross-border payment solution can help your business reduce costs, accelerate settlements, ensure compliance, and deliver seamless international payment experiences.

Get in touch with our experts today to learn more.

Frequently Asked Questions

Q1: What are cross-border payments?

A: Cross-border payments are transactions where funds move between parties located in different countries.

Q2: How long do cross-border payments take?

A: Settlement times range from a few minutes to several business days depending on the payment method and destination country.

Q3: Are cross-border payments safe?

A: Yes. Payments processed through regulated financial institutions and trusted payment providers are generally secure and protected by compliance controls.

Q4: What is the cheapest way to send international payments?

A: The most cost-effective option depends on the transaction amount, destination country, exchange rates, and provider fees.

Q5: Do Indian businesses need RBI approval for every international payment?

A: Most routine business transactions do not require direct RBI approval but must comply with RBI guidelines and FEMA regulations.

Q6: What are the biggest challenges in cross-border payments?

A: Common challenges include high fees, currency fluctuations, compliance requirements, settlement delays, and fraud risks.

Q7: How can businesses reduce cross-border payment costs?

A: Businesses can compare providers, optimize payment routes, reduce intermediary fees, and monitor exchange rate margins.

Q8: Which industries use cross-border payments the most?

A: eCommerce, SaaS, marketplaces, travel, outsourcing, freelancing, import-export, and financial services rely heavily on cross-border payments.

Hyderabad (HQ)

Hyderabad (HQ)