Cross-border payments in India: challenges, costs, and compliance in 2026

India’s cross-border payments landscape is changing fast in 2026. Businesses now expect faster settlement, transparent FX, and simpler compliance, but the reality is still shaped by regulatory complexity, hidden costs, and documentation-heavy processes. For exporters, SaaS companies, freelancers, and importers, the challenge is not just sending or receiving money internationally, but doing it in a way that is cost-effective, compliant, and scalable.

The Rise of Cross-Border Payments

India’s cross-border payment volumes are exploding, with inward remittances hitting a record $135 billion in FY25, the world’s highest, and outward flows growing 17% year-on-year. IT and services exports contribute heavily, alongside rising tourism spend (9.7 million international arrivals in 2024-25, over ₹3 trillion) and gig economy remittances.

RBI’s Payment Vision 2028, building on 2025 goals, targets G20-aligned improvements in speed, cost, and transparency, with UPI expanding globally via Project Nexus (linking to Singapore, UAE, etc., for <60-second settlements). Businesses now handle diverse flows: export receipts ($132.5B services surplus), vendor payments, and freelance income, making RBI compliant cross-border payments essential for scale.

Key Challenges Facing Indian Businesses

1. Regulatory complexity and documentation burden: Navigating FEMA purpose codes, obtaining FIRCs, managing GST on forex transactions, and meeting evolving RBI requirements demand constant attention.

2. Hidden costs and opaque pricing: Between forex markups, correspondent bank deductions, and layered service fees, the actual cost of a cross-border transaction is rarely transparent at initiation. Businesses often discover the true cost only after settlement.

3. Multi-day settlement delays: Traditional SWIFT-based transfers can take 2–5 business days under normal conditions and longer when compliance checks, intermediary routing, or time-zone differences introduce friction.

4. Fraud and Business Email Compromise (BEC): Indian businesses are increasingly targeted by BEC scams related to international invoices. Sending money across borders without robust verification workflows exposes companies to significant financial risk.

5. Technology integration gaps: Reconciling cross-border payments with Indian accounting software like Tally or Zoho Books remains a technical challenge. Ensuring seamless data flow between payment platforms and ERP systems is critical but often overlooked.

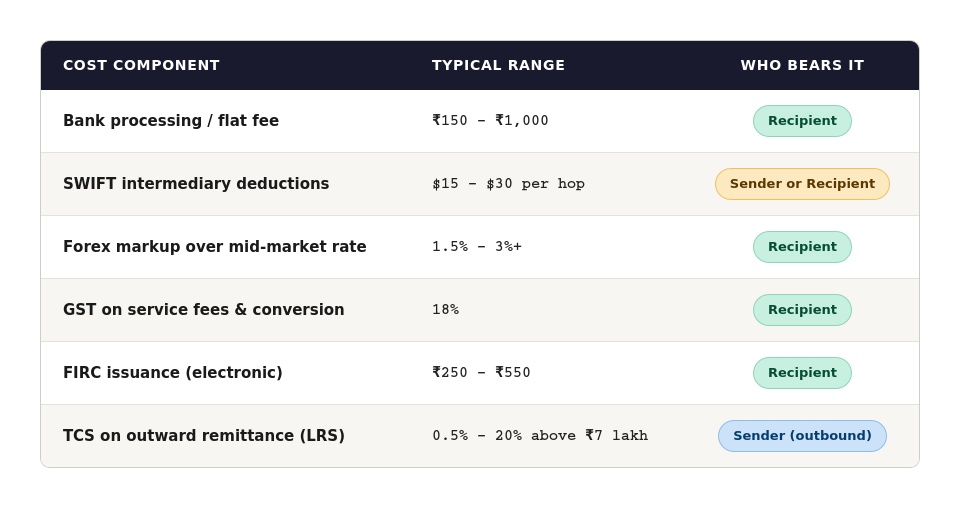

The Real Cost of Cross-Border Payments in India

For Indian businesses, the cost of receiving or sending international payments remains a significant pain point. The total expense is rarely a single line item; it’s a stack of charges that compounds at every stage of the transaction chain.

To put this in perspective: a ₹10,00,000 inward transfer can lose ₹35,000 to ₹50,000—or 3.5% to 5%—to the combined effect of bank fees, intermediary deductions, forex spreads, and taxes. The forex markup alone, typically 1.5% to 3% above the interbank rate, is often the single largest hidden cost, and it doesn’t appear as a separate charge on your bank statement.

Compliance Checklist for 2026

For any Indian business handling cross-border payments, staying compliant requires attention to several evolving requirements:

🔹 Route transactions through a licensed PA-CB: All cross-border payment flows must pass through an RBI-authorised Payment Aggregator–Cross Border entity. Using unlicensed intermediaries exposes your business to regulatory risk.

🔹 Maintain accurate FEMA purpose-code tagging: Every inward and outward remittance must carry the correct purpose code (e.g., P0802 for software services, P0805 for consulting). Incorrect codes cause delays and invite scrutiny.

🔹 Complete KYC and AML documentation: Full Know Your Customer verification is mandatory for all parties. Registration with the Financial Intelligence Unit–India (FIU-IND) is required for PA-CB entities, and suspicious transaction reporting is non-negotiable.

🔹 Preserve your FIRCs: Foreign Inward Remittance Certificates are essential for GST refund claims and proving the export nature of income. Ensure your banking partner provides e-FIRCs promptly.

🔹 Account for TCS on outward remittances: Any remittance under LRS above ₹7 lakh per financial year attracts TCS at varying rates. Budget for this and track cumulative remittances carefully.

🔹 Implement security best practices: PA-CBs must adhere to PCI-DSS and PCI-SSF standards. Annual system audits by CERT-In empanelled auditors, biannual vulnerability assessments, and segregated escrow accounts for inward and outward transactions are all part of the current mandate.

Emerging Trends and Solutions

2026 sees adoption of stablecoin pilots, API-driven orchestration, and RBI-linked faster payments. Businesses benefit from platforms offering:

▪️ Multi-currency virtual accounts for collections.

▪️ Real-time FX hedging.

▪️ Automated compliance workflows.

ToucanPay exemplifies this with its cross-border payment gateway for Indian businesses.

Simplify your international payments with ToucanPay

Lower fees. Faster settlement. Full RBI and FEMA compliance built in. See how ToucanPay helps Indian businesses move money across borders without the friction.

Frequently Asked Questions

Q1: What are the main costs in cross-border payments?

A: Primarily FX markups, bank fees, and intermediaries.

Q2: How does RBI regulate international payments?

A: Via FEMA, purpose codes, and systems like PA-CB for aggregators.

Q3: Can freelancers use cross-border gateways?

A: Yes, for compliant inward remittances with e-FIRA support.

Q4: What’s new in 2026 compliance?

A: Faster credits, updated FEMA regs, and stricter PA-CB oversight.