What Are Cross-Border Payments? How They Work, Costs, and the Best Solutions for Indian Businesses

Cross-border payments are financial transactions where the payer and recipient are located in different countries. This includes an Indian SaaS company collecting subscription fees from a US client, a freelancer receiving payment from a European agency, or an exporter settling invoices with an overseas buyer. These transactions require currency conversion, compliance checks, and routing across multiple banking systems — each adding cost and time.

The global cross-border payments market processed over $190 trillion in 2023 and is expected to exceed $290 trillion by 2030, driven by the rise of digital commerce, remote work, and global supply chains. For Indian businesses, cross-border receipts are governed by FEMA regulations and require proper documentation like FIRC/FIRA certificates — adding a compliance layer that domestic payments don’t have.

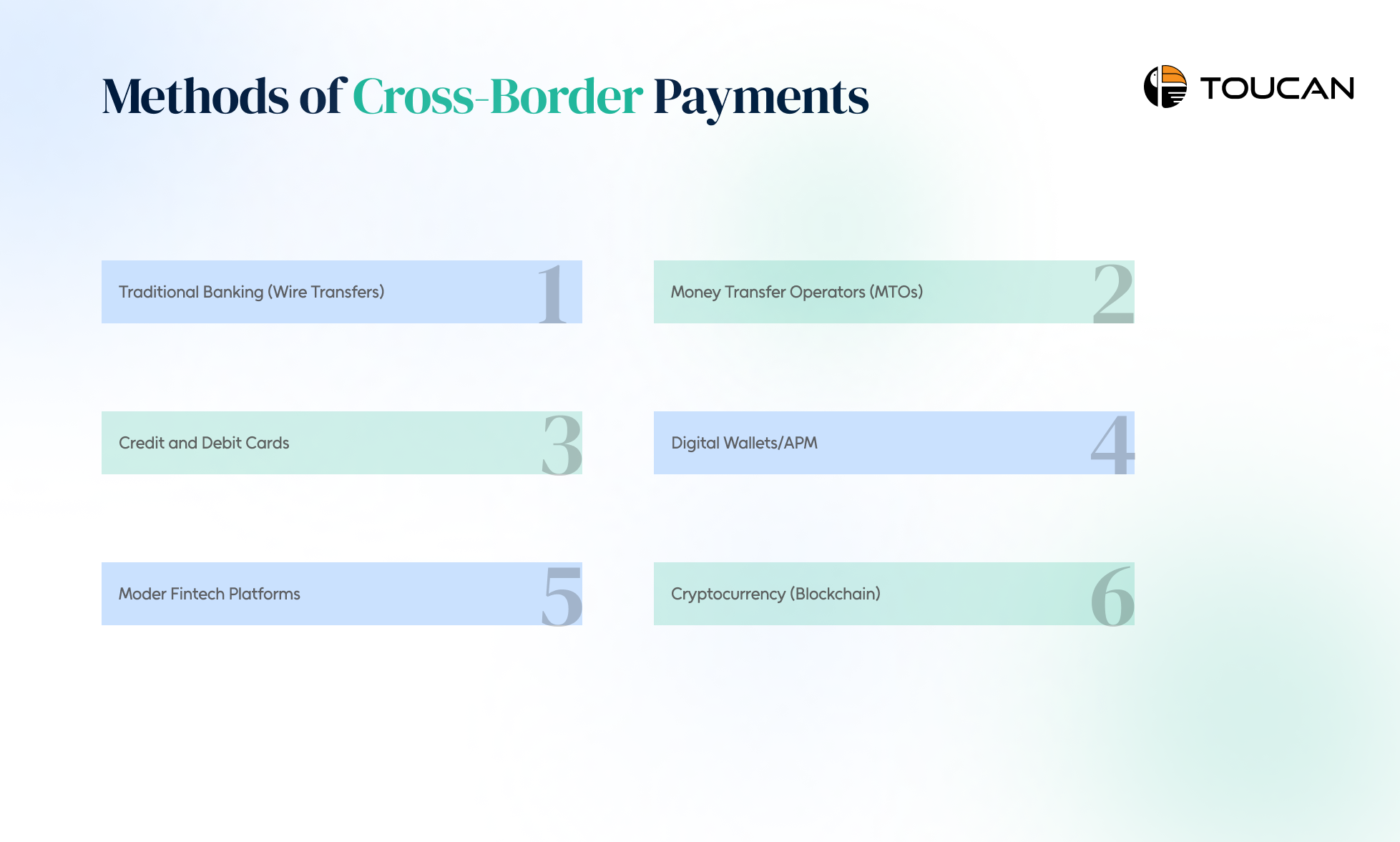

Methods of Cross-Border Payments

➤ Traditional Banking (Wire Transfers) Banks use networks like SWIFT to send money internationally. You provide recipient details to your bank, which routes the payment through correspondent banking relationships.

➤ Money Transfer Operators (MTOs) Companies like Western Union and MoneyGram specialize in person-to-person transfers, often offering cash pickup options in the destination country.

➤ Credit and Debit Cards International card networks (Visa, Mastercard) enable cross-border purchases and payments, though they typically involve currency conversion fees.

➤ Digital Wallets/APM Wallets (PayPal-type services, regional wallets) allow users to hold balances and send/receive cross-border via underlying rails.

➤ Modern Fintech Platforms Services like Toucan Payments allow digital transfers with lower fees and faster processing than traditional banks.

➤ Cryptocurrency (Blockchain) Emerging digital currencies like Stablecoins can facilitate borderless transactions through blockchain network, the adoption for mainstream commerce is at nascent stage as of now.

How cross-border payments work?

1. Initiation

- Sender instructs a bank or PSP (via online banking, API, or platform) to send funds to a foreign beneficiary.

- Key details collected: beneficiary name, account/IBAN, bank details (SWIFT/BIC, routing codes), amount, currency, and payment purpose.

- The provider quotes fees and FX rate (transparent or embedded in the spread), and the sender confirms.

2. Funding and FX conversion

- Sender’s account is debited in the source currency.

- FX can occur at:

- The sending bank/PSP (pre-funding in destination currency).

- An intermediary FX provider.

- The receiving side, if funds are sent in one currency but credited in another.

3. Routing and correspondent banking

- If the sender’s and receiver’s banks do not have a direct relationship, intermediary/correspondent banks bridge the gap.

- The payment message travels across the network, with each intermediary adjusting its ledger and forwarding the payment onward.

4. Compliance, screening, and risk checks

- At multiple points, the payment is screened for:

- AML (suspicious activity, unusual patterns).

- Sanctions lists (restricted individuals, entities, or countries).

- Fraud indicators (mismatched data, unusual behaviour).

For Indian businesses, this step also includes FEMA purpose code validation and generation of the Foreign Inward Remittance Certificate (FIRC/FIRA) — a mandatory document for GST refund claims and RBI reporting.

5. Clearing and settlement in the destination country

- Once the payment reaches the last bank in the chain, it enters the local clearing system (ACH, RTGS, instant payment rail).

- Funds are settled between banks via their accounts (nostro/vostro or central bank accounts), then the beneficiary bank credits the customer account.

6. Confirmation and reconciliation

- The beneficiary receives credit and usually a notification from their bank or PSP.

- The sender may receive confirmation via status updates or statements; richer standards allow tracking (e.g., “in progress,” “credited,” “rejected”).

What Are the Benefits and Challenges of Cross-Border Payments?

Cross-border payments enable businesses to expand globally, reach new markets, and move money beyond borders with ease. However, they also come with challenges like regulatory complexity, high costs, and settlement delays that impact speed and efficiency.

Benefits of cross-border payments:

🔹Global Commerce Enablement: Businesses can easily operate internationally, accessing suppliers and customers worldwide without geographic limitations.

🔹Economic Opportunity: Migrant workers can support families in their home countries through remittances, which represent a significant income source for many developing nations.

🔹Increased Affordability: Multiple payment options have driven down costs and improved service quality compared to the historical monopoly of traditional banks.

🔹Speed: Modern platforms settle in minutes to hours; the G20’s cross-border payments roadmap targets end-to-end payment completion within 1 hour for retail transactions by 2027.

🔹Transparency: Many newer services provide real-time tracking and upfront fee disclosure, eliminating hidden charges.

Challenges of cross-border payments:

🔹High Costs: The global average cost to send $200 internationally was 6.35% in Q1 2024 (World Bank), more than double the UN’s 3% target. Bank wire transfers remain the most expensive channel at ~10–14% all-in cost.

🔹Slow Processing: Legacy banking infrastructure can take 3-5 business days for settlements, creating cash flow issues for businesses and delays for individuals.

🔹Currency Volatility: Exchange rate fluctuations between initiation and completion can affect the final amount received, creating uncertainty for both parties.

🔹Regulatory Complexity: Each country has different financial regulations, compliance requirements, and reporting obligations. Navigating these creates administrative burden and can cause delays.

🔹Fraud and Security Risks: Cross-border transactions are targets for scams, money laundering, terror financing, and fraud, requiring robust security measures that can add friction to legitimate transactions.

🔹Lack of Standardization: Different countries use different payment systems and standards, requiring complex integration and making interoperability challenging.

The Future of Cross-Border Payments

Several structural changes are reshaping how money moves across borders:

➜ ISO 20022 adoption — The global migration to this richer payment messaging standard (underway across SWIFT and RBI) will enable better tracking, fewer rejections, and faster correspondent banking.

➜ Central Bank Digital Currencies (CBDCs) — India’s Digital Rupee (e₹) pilot and similar projects in 130+ countries are exploring direct central bank settlement lanes that bypass correspondent banking entirely.

➜ Real-time gross settlement linkages — India’s UPI has already linked with Singapore’s PayNow and the UAE’s payment rails. More bilateral linkages are expected through 2026–27, reducing cost and time on priority corridors.

➜ Stablecoins for B2B settlement — USD-pegged stablecoins are gaining traction for treasury and supplier payments, particularly in corridors with thin banking coverage.

Ready to take your business global with seamless, compliant, and cost-effective payments? Explore Toucan Payment’s Cross-Border Payment Solutions today!

Frequently asked Questions

Q1: How long do cross-border payments typically take?

A: Traditional bank wire transfers usually take 3-5 business days. Modern digital payment platforms like Toucan Payments or Wise can complete transfers within minutes to 24 hours. The speed depends on the payment method, currency corridor, banking relationships, compliance checks, and time zone differences.

Q2: How can businesses reduce cross-border transaction fees?

A: To reduce fees, businesses can use modern payment platforms that offer transparent FX rates and lower transfer costs. Additionally, using multi-currency accounts can help avoid conversion fees for every transaction.

Q3: Are cross-border payments safe?

A: Reputable payment providers use bank-level encryption, multi-factor authentication, and fraud detection systems to protect transactions. However, you should only use licensed and regulated payment services, verify recipient details carefully to avoid scams.

Q4: What’s the best cross-border payment solution for small businesses?

A: The best solution depends on your specific needs, but popular options include Toucan Payments for Business (low fees, transparent pricing). Consider factors like transaction volume, currencies needed, integration with your accounting software, and the countries you deal with most frequently.