Top 7 Things Indian Businesses Check Before Choosing a Cross-Border Payment Provider

Expanding internationally is no longer limited to large enterprises. Today, Indian exporters, SaaS companies, marketplaces, manufacturers, consulting firms, and D2C brands regularly receive and send payments across borders.

But accepting international payments isn’t just about finding a provider that supports multiple currencies. Hidden foreign exchange charges, delayed settlements, compliance requirements, and limited payment methods can directly impact your cash flow and customer experience.

Choosing the wrong cross-border payment partner may increase operational costs, create reconciliation challenges, and slow business growth.

This guide explains the seven key factors Indian businesses should evaluate before selecting a cross-border payment provider in 2026.

What is a Cross-Border Payment Provider?

A cross-border payment provider enables businesses to send and receive payments between different countries while managing currency conversion, payment processing, settlement, regulatory compliance, and transaction reporting. Modern providers also offer APIs, multi-currency support, fraud protection, and faster settlements for global businesses

How Does a Cross-Border Payment Provider Work?

❶ Customer makes an international payment.

❷ Payment is verified.

❸ Currency conversion takes place.

❹ Compliance checks are completed.

❺ Funds are routed through banking or payment networks.

❻ Amount is settled into the business account.

❼ Reports and reconciliation data become available.

7 Factors to Consider When Choosing a Cross-Border Payment Provider in India

1. Transparent Pricing and Foreign Exchange Rates

This is often the first thing finance teams evaluate.

Many providers advertise low transaction fees but recover revenue through foreign exchange markups, intermediary bank charges, or settlement fees.

Before signing up, ask:

⬢ Is the FX markup fixed?

⬢ Are there hidden charges?

⬢ Is pricing corridor-specific?

⬢ Are refunds charged separately?

⬢ Are settlement fees applicable?

Instead of comparing only transaction fees, calculate the total cost of receiving $10,000 or €20,000 through each provider.

2. Countries and Currency Coverage

Not every provider supports every market equally.

One provider may perform exceptionally well for payments from the US while another offers better coverage across Europe or the Middle East. Experts increasingly recommend evaluating providers by payment corridor rather than assuming one platform fits every geography.

Questions to ask:

⬢ Which countries are supported?

⬢ Which currencies can customers pay in?

⬢ Are local payment methods available?

⬢ Can payouts be made globally?

3. Settlement Speed

Cash flow matters.

Waiting several business days for international payments can affect supplier payments, payroll, and working capital.

Look for providers offering:

⬢ Same-day settlements

⬢ Next-day settlements

⬢ Real-time tracking

⬢ Instant payment notifications

Settlement timelines can differ depending on payment method and country corridor.

4. Regulatory Compliance

Compliance should never be an afterthought.

Indian businesses must comply with:

⬢ FEMA regulations

⬢ RBI guidelines

⬢ KYC verification

⬢ AML screening

⬢ Documentation requirements

Modern providers increasingly automate much of this process, reducing manual effort and helping businesses stay compliant

5. Payment Methods Supported

Customers prefer paying through methods they already trust.

A flexible provider should support:

The more payment options available, the lower the chances of checkout abandonment.

6. API Integration and Automation

Growing businesses shouldn’t rely on manual payment processing.

Look for:

⬢ REST APIs

⬢ SDKs

⬢ Webhooks

⬢ ERP integrations

⬢ Accounting integrations

⬢ Automated reconciliation

⬢ Dashboard reporting

Strong APIs reduce manual work while making payment operations easier to scale.

7. Security and Fraud Protection

Cross-border payments carry additional fraud risks.

Check whether the provider offers:

⬢ PCI DSS compliance

⬢ Encryption

⬢ Tokenization

⬢ AI fraud detection

⬢ Transaction monitoring

⬢ Risk scoring

Security should protect both your business and your customers.

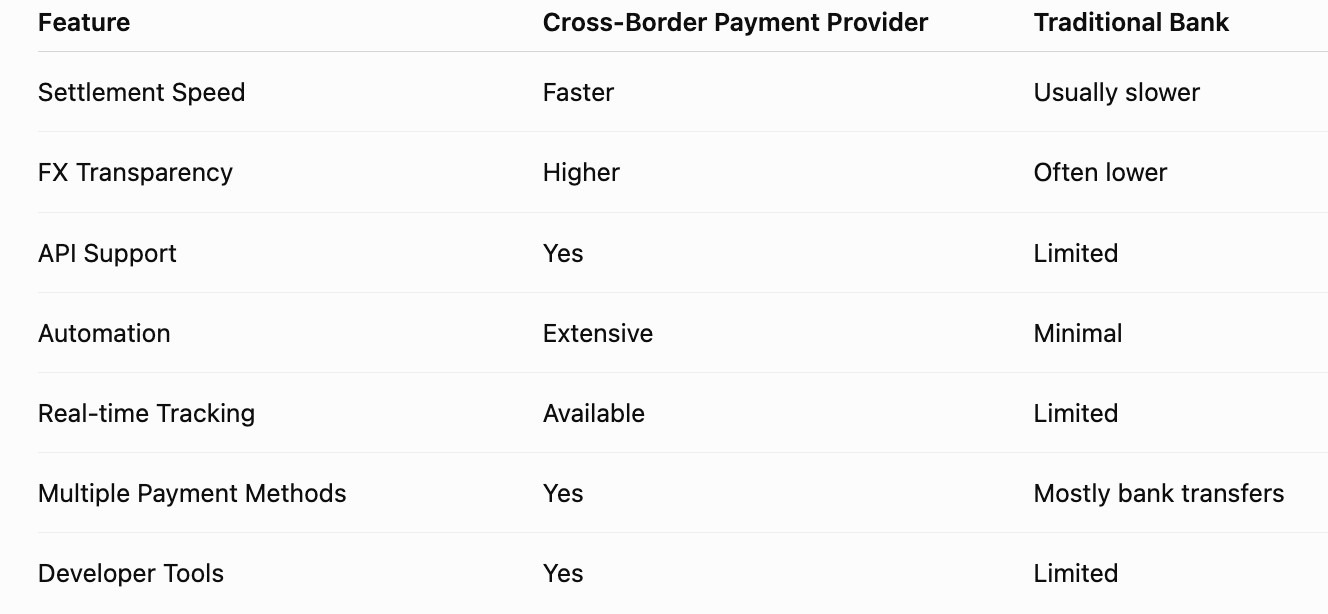

Cross-Border Payment Provider vs Traditional Bank

Both traditional banks and cross-border payment providers enable international payments, but they differ in cost, speed, flexibility, and technology. The table below highlights the key differences.

Mistakes to Avoid When Choosing a Cross-Border Payment Provider

Even the best payment provider may not be the right fit if important evaluation criteria are overlooked. Here are some common mistakes businesses should avoid before making a decision.

⬢ Comparing only transaction fees

⬢ Ignoring FX markups

⬢ Overlooking settlement timelines

⬢ Choosing a provider with limited country coverage

⬢ Not checking API capabilities

⬢ Ignoring compliance support

⬢ Focusing only on brand popularity instead of business fit

Conclusion

Choosing the right cross-border payment provider goes beyond comparing transaction fees. Evaluate factors like transparent pricing, settlement speed, currency coverage, compliance, security, payment methods, and API capabilities to find the best fit for your business. A reliable provider can help reduce costs, improve cash flow, and support your global growth with confidence.

Related reads:

Cross-Border Payments in India: 2026 Guide

Cross-Border Payments: How They Work, Types & What Indian Businesses Need to Know

Frequently Asked Questions

Q1: What is the most important factor when choosing a cross-border payment provider?

A: Pricing transparency, regulatory compliance, settlement speed, country coverage, and security are among the most important factors.

Q2: How do cross-border payment providers make money?

A: They typically earn through transaction fees, foreign exchange markups, subscription plans, and value-added services.

Q3: How long do international business payments take?

A: Settlement can range from a few minutes to several business days, depending on the payment corridor, method, and provider. Faster payment rails are improving these timelines, but performance still varies by country pair.

Q4: Can Indian businesses receive payments in multiple currencies?

A: Yes. Many providers support receiving payments in USD, EUR, GBP, AED, SGD, and several other currencies.

Q5: Are cross-border payment providers regulated?

A: Yes. Reputable providers operate under relevant financial regulations and licensing requirements in the jurisdictions they serve.

Q6: Do all providers support APIs?

A: No. Enterprise-focused providers generally offer APIs, webhooks, and automation tools, while smaller providers may have limited integration capabilities.

Q7: How can businesses reduce international payment costs?

A: Compare the total cost—including FX spreads, transaction fees, settlement charges, and any hidden fees—rather than looking only at the advertised processing fee.

Q8: Is a bank or a payment provider better for international business payments?

A: It depends on your needs. Traditional banks may suit occasional transfers, while dedicated cross-border payment providers often offer better pricing transparency, automation, and faster settlement for businesses with regular international transactions.

Hyderabad (HQ)

Hyderabad (HQ)