Cross-Border Payment Costs: The Complete Breakdown for Indian Businesses (FX, SWIFT, Hidden Fees)

Sending ₹1,00,000 internationally shouldn’t cost ₹8,000 to ₹12,000 in fees. Yet for millions of Indian businesses, freelancers, and importers, that’s the quiet reality of the global banking system. Cross-border payment costs are layered, opaque, and deliberately complicated.

Whether you’re a startup paying international vendors, a freelancer receiving USD payments, or a business managing import invoices, understanding the cost anatomy of a cross-border transaction is the first step to controlling it.

Let’s break it down, layer by layer.

FX Conversion Costs Explained

Foreign Exchange (FX) markups

The largest CB cost embedded when providers quote rates above the mid-market (RBI reference) rate. A bank might quote you ₹83.10 to the dollar when the real rate is ₹84.50. That ₹1.40 gap, spread across a ₹10 lakh transaction, silently costs you ₹16,500.

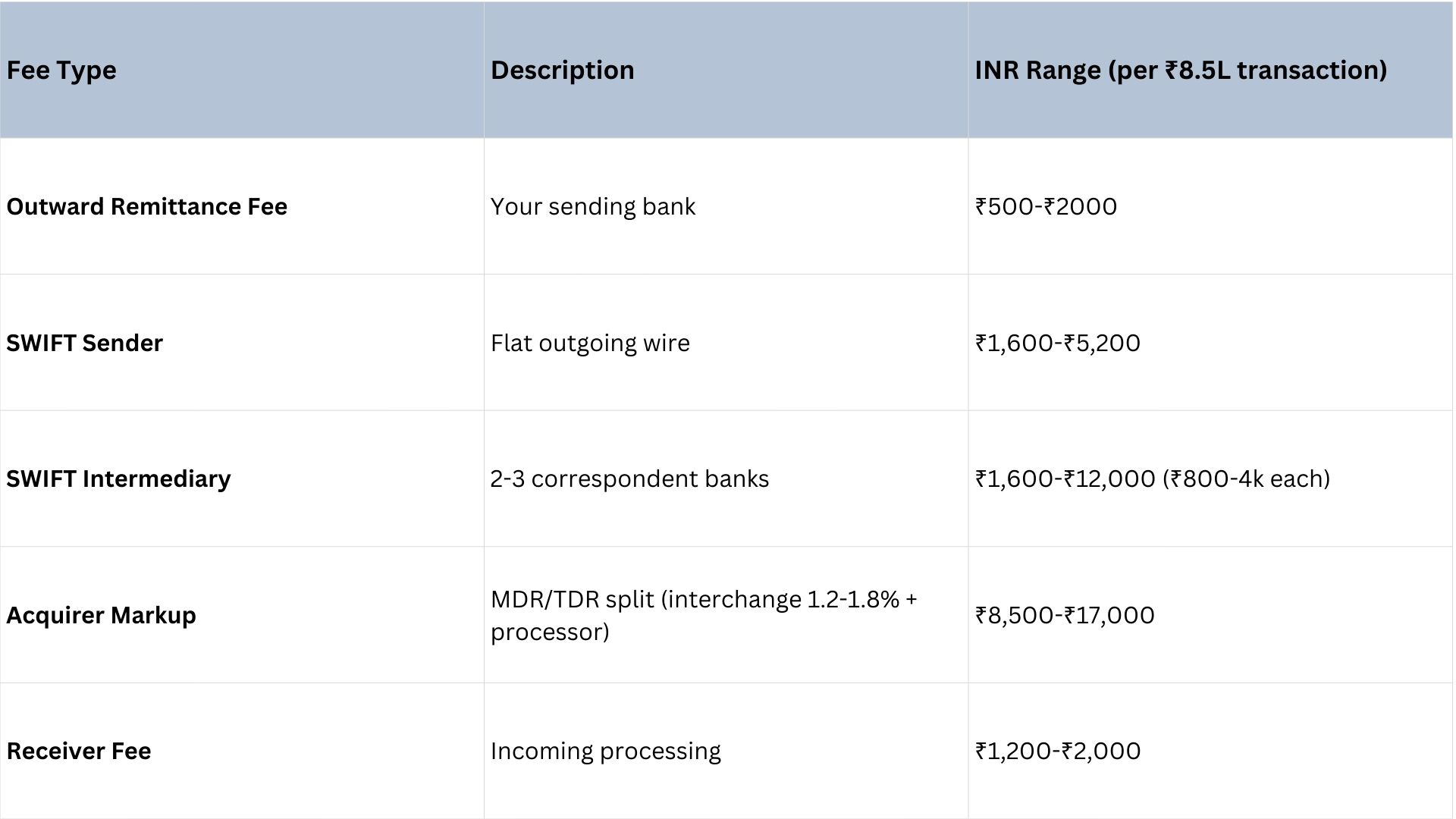

Network and Processing Fees

An international wire transfer doesn’t go directly from your bank to the recipient’s bank. It travels through a network of intermediary banks called correspondent banks, each operating as a relay station. And each one charges for the privilege.

Hidden Charges That Multiply Costs

Often deducted post-settlement, these evade initial quotes:

- GST on Services: 18% on gateway/processor fees (₹1.5k-₹3k).

- TDS/FEMA Penalties: 1-20% on import payments; short realization fines.

- Chargebacks/Disputes: ₹5k-₹20k + 1-2% liability.

- Card Extras: Dynamic currency conversion (DCC) forces 5-7% loss vs. local card.

How to Minimise Cross-Border Payment Costs: A Practical Guide

Armed with an understanding of where costs come from, here’s how businesses and individuals can systematically reduce them.

✦ Compare exchange rates, not just fees

Most people compare the flat fee (₹500 vs ₹1,000). But the FX margin on a large transaction dwarfs any fixed fee. Always calculate the effective rate.

✦ Use local settlement networks where possible

Modern payment platforms like Toucan use local payment rails that dynamically pick cheapest path (cards/UPI/wallets), boosting approvals 10-40% and cutting costs 10-40%.

✦ Batch your payments strategically

Fixed fees (like SWIFT charges) make small, frequent transfers expensive. Where possible, consolidate multiple smaller payments into larger, less frequent batches to reduce the per-transaction overhead.

✦ Lock in rates for predictable flows

If you regularly receive USD or EUR payments, consider locking in forward contracts or using a platform that offers rate holds. This protects against INR depreciation eating into your margins between invoice and settlement.

✦ Avoid airport kiosks and hotel forex counters

For travellers, airport forex desks routinely apply 5–8% margins. Use a multi-currency card or a travel-friendly platform that applies near-interbank rates.

Conclusion

The international payments industry has been built on information asymmetry, most businesses simply don’t know how much they’re overpaying, and traditional banks have little incentive to change that. Understanding the three-layer cost structure (FX markup, network fees, and hidden charges) is the first and most important step to taking control.

However, the landscape is changing. Platforms built for modern Indian businesses are offering transparent rates, local settlement infrastructure, and honest pricing, making it increasingly easy to stop subsidising the correspondent banking network.

At Toucan, we believe every rupee of your hard-earned foreign income should reach your account.

Ready to take your business global with seamless, compliant, and cost-effective payments?

Explore Toucan Payment’s Cross-Border Payment Solutions today!

Frequently Asked Questions

Q1: What are the main components of cross-border payment costs?

A: FX markups (2-5%), network fees (1-2% Visa/MC or ₹800-4k SWIFT), and hidden charges like spreads/GST (1-3%) total 4-7% per transaction.

Q2: Does RBI regulate cross-border payment costs?

A: Yes, 2025 draft mandates total-cost disclosure; authorized aggregators must comply. Liberalised Remittance Scheme caps USD 250k/year with transparency.

Q3: How does volume affect negotiated rates?

A: High-volume (₹10Cr+/month) unlocks 0.3-0.8% FX + capped fees; batching amplifies leverage with aggregators.