AI-Powered Fraud Detection: How Machine Learning Stops Payment Fraud before it happens

Digital payments are scaling at an unprecedented pace—but so is fraud.

According to ACI Worldwide and Global Data, global payment fraud losses are expected to exceed $40 billion annually by 2027, driven largely by the rise of e-commerce, real-time payments, and cross-border transactions. In India alone, digital payment fraud cases have seen double-digit growth year-on-year, RBI annual report coverage showed fraud cases in the card and internet payment category rose from 6,699 in FY23 to 29,082 in FY24, fuelled by increasing transaction volumes and sophisticated attack vectors.

The reality is simple: as payment systems become faster and more seamless, fraud detection must become smarter and more predictive.

The Rising Complexity of Payment Fraud

Fraud today is no longer opportunistic—it’s engineered.

➤ Card-not-present (CNP) fraud accounts for over 70% of card fraud losses globally, largely due to the growth of online commerce

➤ Account takeover (ATO) attacks increased by ~30% in recent years, driven by credential leaks and automation tools

➤ Friendly fraud and chargebacks can account for up to 60–80% of disputes for some merchants

➤ Cross-border transactions are 2–3x more likely to be flagged as high-risk compared to domestic payments

Traditional rule-based systems, built on static thresholds, fail to keep up with these dynamic threats. They either miss fraud or block legitimate users, leading to revenue loss and poor customer experience.

What Is AI-Powered Fraud Detection?

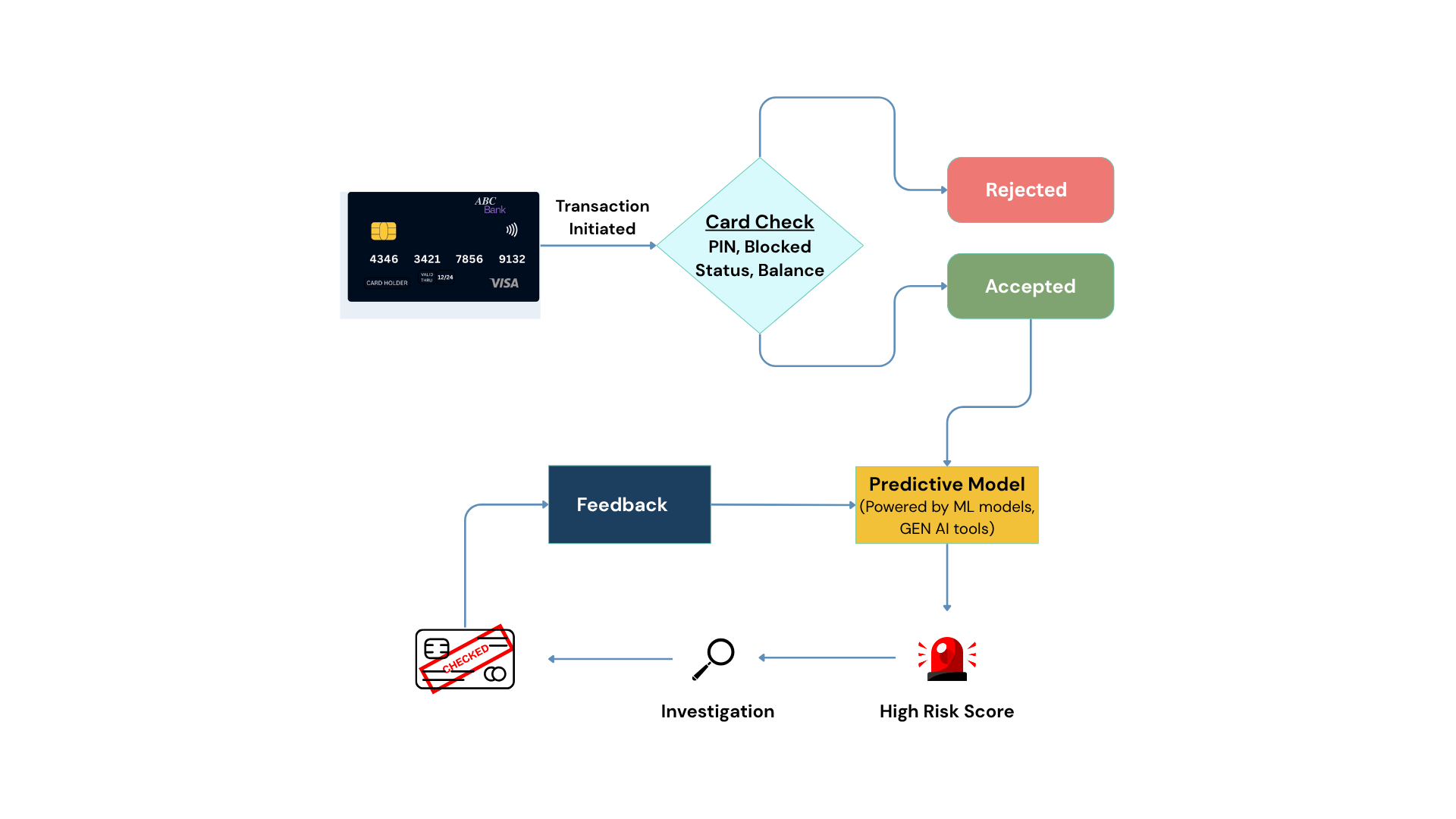

AI-powered fraud detection uses machine learning algorithms to analyse transaction data in real time and predict whether a given payment is fraudulent, before it is authorised.

Instead of following a fixed checklist of rules, ML models learn patterns from millions of historical transactions. They understand what “normal” looks like for each user, merchant category, geography, device, and time of day. Anything that deviates from that learned norm gets flagged, scored, and acted upon instantly.

The result: fraud caught at the point of transaction, not weeks later during a chargeback dispute.

For example, if a user typically spends ₹2,000–₹5,000 locally and suddenly initiates a ₹75,000 international transaction from a new device, AI instantly flags it as anomalous—often within milliseconds.

How Machine Learning Stops Fraud Before It Happens

1. Behavioural Profiling at Scale

Machine learning models continuously build user profiles based on:

✔ Spending behaviour

✔ Device and browser fingerprints

✔ Transaction frequency

✔ Location patterns

2. Real-Time Anomaly Detection

Unlike rule-based systems, ML models detect unknown fraud patterns.

This is critical because over 60% of fraud attacks involve new or previously unseen tactics, making signature-based detection ineffective.

3. Continuous Learning and Adaptation

Fraud evolves daily. AI systems retrain on fresh data, improving accuracy over time.

Organizations using AI-based fraud systems have reported:

✔ 30–50% reduction in fraud losses

✔ 20–40% decrease in false declines

This directly translates into higher approval rates and better customer retention.

4. Real-Time Risk Scoring

Every transaction is evaluated in under 100 milliseconds, enabling instant decisions:

✔ Low-risk → seamless approval

✔ Medium-risk → step-up authentication (OTP, 3DS)

✔ High-risk → transaction blocked

This balance between security and experience is critical, because 32% of customers abandon transactions after a false decline.

5. Network-Wide Intelligence

AI systems don’t operate in isolation, they learn across ecosystems.

If a fraud pattern emerges across a specific BIN range, geography, or merchant category, the system can proactively block similar attempts across the network.

This creates a collective defence layer, far stronger than siloed fraud systems.

Reducing False Positives: The Other Side of the Equation

Here’s the uncomfortable truth that legacy systems ignore: a false positive — blocking a legitimate transaction is also costly.

Imagine a business owner in Jaipur trying to pay a vendor while traveling in Singapore. An old rule-based system might block the transaction outright. The business owner is frustrated, calls the bank, wastes an hour, and potentially loses the deal.

AI solves this with personalization. The model knows this particular customer regularly travels internationally, has made large vendor payments before, and their device fingerprint matches. The transaction goes through — without friction, without a blocked card, without a frustrated customer.

This is the balance good ML fraud detection strikes: high fraud catch rate AND low false positive rate. Both matter. Both are achievable with the right model.

The Road Ahead: Predictive and Autonomous Fraud Prevention

We’re moving toward a future where fraud prevention systems:

1️⃣ Predict fraudulent intent before transaction initiation

2️⃣ Integrate deeply with digital identity and KYC systems

3️⃣ Use graph intelligence to detect fraud rings and networks

4️⃣ Operate autonomously with minimal human intervention

In this landscape, payments platforms that leverage AI will not just reduce fraud—they’ll unlock higher approval rates, better user experiences, and stronger trust.

At Toucan Payments, we’re building intelligent payment infrastructure where every transaction is not only seamless, but secure by design.

Frequently Asked Questions

Q1: What is AI-powered fraud detection?

A: AI-powered fraud detection uses machine learning models to analyse transaction patterns, user behaviour, device signals, and anomalies in real time to identify suspicious activity before a payment is completed.

Q2: Why is AI better than rule-based fraud detection?

A: Rule-based systems depend on fixed conditions, while AI can adapt to new fraud patterns and improve detection as it processes more data.

Q3: What are the most common types of payment fraud?

A: Common types include card-not-present fraud, account takeover, card testing, BIN attacks, APP fraud, gift card fraud, and synthetic identity fraud.

Q4: Can AI reduce false declines?

A: Yes. By combining behavioural analytics, anomaly detection, and richer transaction context, AI can reduce unnecessary blocks on genuine customers while still catching suspicious activity.

Q5: How can businesses improve payment security beyond AI?

A: Businesses can add layers such as 3D Secure, CVV checks, multifactor authentication, tokenization, transaction alerts, and regular security reviews.

Hyderabad (HQ)

Hyderabad (HQ)